Let’s be honest—most people don’t get into RV investing because they love spreadsheets and tax law.

But here’s the truth: savvy investors know the tax benefits of owning a rental RV can be just as valuable as the rental income itself. In fact, understanding how depreciation and write-offs work could be the difference between a break-even hobby and a high-performing investment.

Whether you’re just getting started or already have a few rentals on the road, this guide will walk you through how depreciation works, which expenses you can write off, and how to structure your RV business to keep more of what you earn.

Table of Contents

- What Makes RVs a Tax-Efficient Investment

- How RV Depreciation Works

- Bonus Depreciation: What It Means for You

- Deductible Expenses for RV Investors

- Common Tax Mistakes (and How to Avoid Them)

- Comparing RV and Real Estate Tax Strategies

- Should You Use an LLC for Your RV Rental Business?

- CPA Tips for First-Time RV Investors

- Final Thoughts: Maximize Income, Minimize Taxes

1. What Makes RVs a Tax-Efficient Investment

Here’s the thing most people don’t realize: when you rent out your RV, it’s no longer just a vehicle—it becomes a business asset. That means the IRS allows you to deduct a wide range of expenses, including the depreciation of the RV itself.

Think about that: you're making money and writing off the value of the asset over time.

Some of the biggest tax advantages include:

- Accelerated depreciation (more write-offs, faster)

- Bonus depreciation (potentially huge first-year deductions)

- Everyday expense deductions

- “Paper losses” that reduce your total taxable income

If you're a numbers person, this is where things get fun.

2. How RV Depreciation Works

Let’s break it down simply: RV depreciation is like a tax refund you earn each year, just for using your RV as a rental.

Most RVs are depreciated using something called MACRS (Modified Accelerated Cost Recovery System), over five years. So, if you buy a new RV for $70,000, you might be able to write off about $14,000 a year for five years—even if your RV is still in great shape and making money.

That deduction directly reduces your taxable income. And no, you don’t need to sell the RV to “unlock” the depreciation. It’s built into the asset from day one.

3. Bonus Depreciation: What It Means for You

If you’ve heard about bonus depreciation, here’s what it means in plain English: the government lets you take a big chunk of the depreciation upfront, in the first year.

Under current tax law (thanks to the Tax Cuts and Jobs Act), you can write off:

- 80% of the RV’s value in Year 1 (if placed into service in 2023)

- 60% in 2024

- 40% in 2025

This is especially powerful if you’re trying to offset other high-income sources, like a full-time job or a successful business. It can even help bring your effective tax rate down.

4. Deductible Expenses for RV Investors

Depreciation is great—but it’s just the beginning. Almost everything you spend on your RV rental business is deductible (as long as it’s considered “ordinary and necessary”).

This includes:

- Insurance

- Storage fees

- Repairs and maintenance

- Cleaning supplies

- Listing platform fees

- Fuel (for delivery or prep trips)

- Advertising

- Accounting software or professional services

Stack these on top of depreciation, and you’ve got a powerful tax-saving formula.

5. Common Tax Mistakes (and How to Avoid Them)

Even smart investors make rookie mistakes. Here are a few to avoid:

Pro tip: If you ever use your RV personally, keep a log. That way you stay compliant and still benefit from business-use deductions.

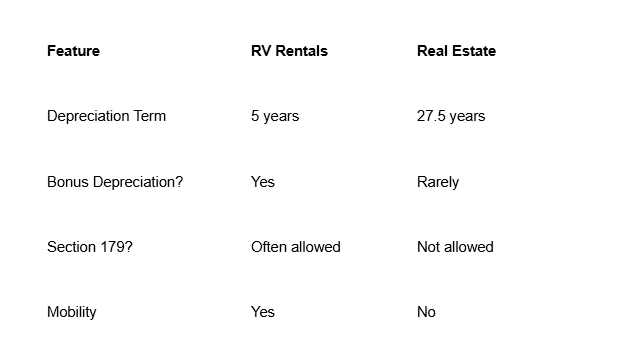

6. Comparing RV and Real Estate Tax Strategies

Here’s how RVs stack up against traditional real estate from a tax standpoint:

Yes, RVs lose value faster than houses—but that means faster write-offs. If you’re trying to shelter income quickly or maximize deductions, RVs can offer surprising advantages.

7. Should You Use an LLC for Your RV Rental Business?

A lot of people ask this: Do I need an LLC to rent out my RV?

The short answer? Not necessarily—but it helps.

Setting up an LLC allows you to:

- Separate personal and business finances

- Limit personal liability

- Deduct startup and operating costs

- Build credibility with banks, insurers, and renters

Just remember: an LLC won’t reduce your taxes on its own. It’s the activity (renting out the RV) that creates the deductions.

8. CPA Tips for First-Time RV Investors

We asked a few tax pros what they’d tell first-time RV investors. Here’s what came up again and again:

“Open a separate business bank account immediately. Don’t mix personal and business funds.”

“Track your mileage—even if it’s just for maintenance trips.”

“You can still deduct losses if this is part-time. Just keep good records and show intent to make a profit.”

9. Final Thoughts: Maximize Income, Minimize Taxes

Here’s the big takeaway: your RV is more than just a weekend getaway—it can be a tax-smart business asset.

With depreciation, bonus write-offs, and deductible expenses, it’s possible to earn solid income while dramatically lowering your tax bill.

You don’t need to be a tax expert to benefit. You just need to treat your RV like a business—and have the right team in your corner.

Want to make sure your RV business is set up for maximum tax efficiency? Contact RV Management USA and get a custom analysis from our expert team.

— RVM Team