Traditional retirement plans include 401(k)s, IRAs, index funds, and sometimes real estate—but what about RV rentals?

For retirees or near-retirees looking for hands-off income, tangible assets, and scalable cash flow, building a portfolio of rental RVs is quickly becoming a smart alternative or supplement to traditional investing. And unlike paper assets, RVs serve both lifestyle and financial goals.

In this article, we’ll explore whether RV rentals make sense as a retirement income plan, and how they compare to more common options like real estate or dividend portfolios.

Table of Contents

- The Retirement Case for RV Rentals

- RVs vs. Real Estate vs. Index Funds

- Passive Income Potential in Retirement Years

- The Power of Consignment and Territory Management

- Risk, Depreciation, and Maintenance Considerations

- Why RVM Makes RV Rental a Smart Retirement Strategy

- Final Thoughts: Investing for Lifestyle and Legacy

1. The Retirement Case for RV Rentals

RV rentals offer a compelling value proposition for retirees:

- Stable monthly cash flow from short-term bookings

- Lower acquisition costs than real estate

- Flexible asset use (use it yourself or rent it out)

- Tangible asset control vs. market-tied volatility

Whether you want a small side income or a multi-RV operation, you control the pace, size, and level of involvement. It’s an investment with lifestyle utility and scale potential.

2. RVs vs. Real Estate vs. Index Funds

RV rentals bridge the gap between real estate and paper assets—offering cash flow like rentals, flexibility like stocks, and utility like a lifestyle asset.

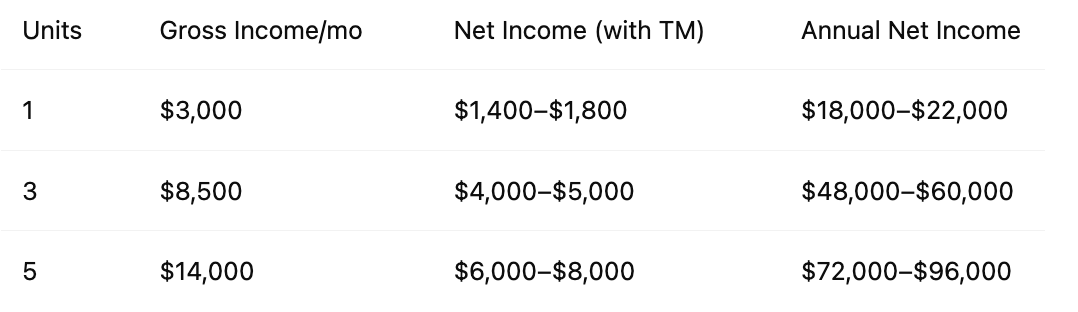

3. Passive Income Potential in Retirement Years

Here’s what a passive RV rental portfolio might look like for a retiree:

These numbers assume 60–70% occupancy, 45–50% revenue share to the owner, and consigned or financed RVs. No hands-on operations required.

4. The Power of Consignment and Territory Management

Retirees don’t want a second job—they want passive cash flow. That’s where RVM’s model comes in.

With territory-based management, retirees can:

- Finance the startup cost (territory + reserves)

- Have RVM deliver and operate up to 10 consigned RVs

- Earn monthly income without managing guests or maintenance

This model allows for regional diversification, predictable revenue, and complete time freedom—ideal for retirees looking to balance travel, income, and legacy planning.

5. Risk, Depreciation, and Maintenance Considerations

No investment is risk-free. With RVs, the biggest concerns are:

- Depreciation – mitigated by high income and early ROI

- Damage or breakdowns – covered by commercial insurance and platform protections

- Seasonality – managed through diversified unit types and flexible locations

But unlike real estate, you’re not tied to a single market. RVs can move where the demand is. And unlike stocks, you’re not at the mercy of macro trends.

6. Why RVM Makes RV Rental a Smart Retirement Strategy

RVM’s platform simplifies everything:

- We source and supply RV units tailored to demand

- We manage guest communications, turnovers, and cleaning

- We provide the software, support, and reporting

All you do is:

- Choose a territory or growth strategy

- Review performance reports monthly

- Collect your income

Whether you want to invest in one rig or ten, RVM gives you a blueprint and a partner to grow your retirement cash flow.

7. Final Thoughts: Investing for Lifestyle and Legacy

RV rental isn’t just about money—it’s about freedom, utility, and building a semi-passive income stream you control.

For many retirees, it’s the perfect hybrid: high-yield, low-involvement, and aligned with lifestyle. You can even involve family, create succession options, and pass on a profitable business.

If your ideal retirement includes financial freedom and adventure, a managed RV rental portfolio may be your next best investment.

– RVM Team