Scaling your RV rental business often comes down to one big question: how do I pay for more RVs without draining my savings?

The good news is, there are multiple ways to finance a growing fleet—each with its own advantages depending on your risk profile, cash flow goals, and timeline. In this guide, we’ll walk through the smartest strategies to acquire and finance multiple RVs so you can grow with confidence.

Whether you're acquiring your second unit or scaling toward ten or more, this article breaks down how to do it without getting financially overextended.

Table of Contents

- Why Financing Beats Paying Cash for Scale

- Traditional RV Loans: Pros, Cons, and Terms

- Business Loans and Commercial Lending

- HELOCs, Cash-Out Refis, and Tapping Home Equity

- Lease-to-Own and Vendor Financing

- Partnering with Capital-Backed Investors

- RVM’s financing path for Territory Managers

- Stacking Strategies for Long-Term Scale

- Final Thoughts

1. Why Financing Beats Paying Cash for Scale

When you're building a rental fleet, your capital should be a lever—not a limit. Paying cash might feel safe, but it restricts your ability to grow. Financing allows you to:

- Expand faster using other people’s money (OPM)

- Spread risk across multiple income-producing units

- Preserve liquidity for maintenance, marketing, or emergencies

If a $70,000 RV generates $3,000/month, and your monthly financing cost is $1,200—you’re in positive cash flow territory.

Financing doesn’t just let you grow. It keeps you liquid and adaptable, especially in seasonal markets.

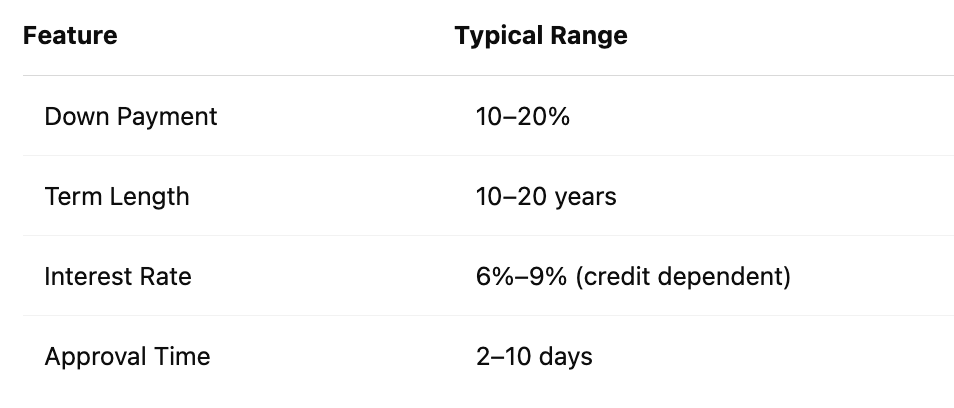

2. Traditional RV Loans: Pros, Cons, and Terms

Most RV owners start here. Banks and credit unions offer secured loans with RV title as collateral.

Pros:

- Predictable monthly payment

- Long terms = lower cash burden

- Easy to qualify if you have good credit

Cons:

- Debt tied to personal name (unless through business)

- May limit total units you can carry before credit ceiling hits

- Can impact personal DTI (debt-to-income) ratio

Tip: Use a lender familiar with RV rentals (or be upfront about your intent) to avoid complications.

3. Business Loans and Commercial Lending

As your operation matures, business lending becomes a scalable option.

Options include:

- Equipment financing (secured by the RV)

- SBA loans (if structured as a formal business)

- Business lines of credit (for flexible access)

Pros:

- Keeps debt off your personal credit

- Builds business credit profile

- Often allows faster repeat expansion

Cons:

- May require 1–2 years of operating history

- Higher documentation requirements

- Often needs stronger cash flow underwriting

If you plan to own 5+ RVs, talk to a business banker early—many lenders love recurring-revenue models with asset-backed risk.

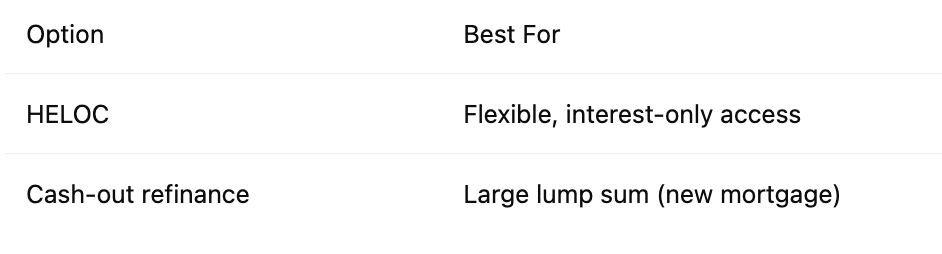

4. HELOCs, Cash-Out Refis, and Tapping Home Equity

Have equity in your home? You may already be sitting on capital.

These strategies are ideal if you:

- Want to maintain full ownership of the RV (no debt on it)

- Have great home equity (>30%)

- Don’t want multiple new loans

Caution: Only use home equity if the ROI on your RV portfolio clearly beats the cost of funds. Don’t gamble with your house unless the math is bulletproof.

5. Lease-to-Own and Vendor Financing

Some RV dealerships offer in-house lease or financing packages, especially for commercial buyers.

Advantages:

- Often lower upfront cost

- More flexible underwriting

- Structured for short-term ownership or eventual buyout

These are especially useful if you:

- Want to test a model before full commitment

- Don’t want long-term financing on paper

- Need to expand quickly while preserving flexibility

Always read the fine print. Lease-to-own programs can carry higher APRs or hidden fees.

6. Partnering with Capital-Backed Investors

Want to scale without using your own credit or capital? Consider a partner.

These investors may:

- Fund the RV purchase

- Own the unit outright or jointly

- Share revenue based on performance

Example deal structure:

- Investor buys a $70K RV

- You manage and operate it

- Split: 50% investor / 40% manager / 10% platform (RVM)

Benefits:

- No upfront cost for you

- Shared downside risk

- Repeatable model for scaling

This is the model used by many territory managers in the RVM network. Once your system works, investors are often eager to fuel more units.

7. RVM's Financing Path for Territory Managers

If you're aiming to scale but need help financing the entry point, RVM offers a solution for prospective Territory Managers who qualify.

We’ve partnered with third-party financing providers who can help cover the initial territory fee—so you don’t have to fund it all upfront out of pocket. This unlocks the ability to start your own managed rental operation even if your current capital is limited.

Here’s how it works:

- RVM helps you get financed for the territory fee (subject to approval)

- You secure your exclusive territory with a clear roadmap to ROI

- We bring up to 10 consigned RV units in your first year

- You operate the units using RVM’s backend systems, guest workflows, and support structure

This model enables fast, low-risk scaling with zero RV purchases upfront. You focus on management and growth—we help you source the fleet and streamline the operation.

Key benefits:

- No need to purchase RVs out of the gate

- Minimal capital required to get started

- RVM provides training, software, and fleet strategy

- Up to 10 high-performing units consigned into your territory in Year 1

If you’re serious about scaling without draining your savings—or you want to grow a full-time RV business with professional support—this is the model to consider.

8. Stacking Strategies for Long-Term Scale

Here’s how successful owners grow from 1 unit to 10+ without collapsing under debt or risk:

- Start with a traditional RV loan for unit #1

- Use cash flow to build a track record

- Add a second unit via HELOC or small business loan

- Introduce a lease-to-own model with a dealership partner

- Bring in investors for units 4–10 under revenue-share

This hybrid stack keeps you diversified across:

- Personal and business credit

- Fixed and variable repayment structures

- Owned and operated vs. investor-backed units

8. Final Thoughts

Financing multiple RVs isn’t just about getting loans—it’s about structuring your capital to maximize returns and minimize risk.

With smart planning, you can:

- Acquire 3–5 RVs with minimal personal capital

- Maintain liquidity for emergencies and maintenance

- Build a system that scales into a true business—not a second job

At RV Management USA, we work with growth-minded owners to structure financing, revenue-share partnerships, and territory models that let you expand with confidence.

Let your capital work for you. Let your systems run for you. And let the RVs fund themselves.

– RVM Team